How To Beat Credit Card Float

Credit cards can be a powerful financial tool. Used properly, a credit card account helps build your credit scores and provides access to many other benefits from consumer protections to rewards points to cash back. But with great power comes great responsibility. The average American has not mastered the use of credit cards and carries over $5,000 of credit card debt. It's easy to understand why. Credit cards are designed to encourage spending too much money. In this article we'll take a look at how credit card bills work, what is credit card float, and how to get out of it.

What Is Credit Card Float?

Anytime you need to use your credit card because you don't have the cash to pay for something, you're riding the float. Essentially, credit card float is when you depend on using credit cards instead of cash to make ends meet. It's spending money you haven't yet earned. It's borrowing against your future income to pay for all the spending of the past. It's negative cash flow. The float is dangerous because it can trick you into feeling more financially secure than you really are.

How Do I Know If I'm Riding Credit Card Float?

There are two simple ways to know if you're riding credit card float: (1) If the amount in your checking account is lower than your credit card balance, you are riding credit card float or (2) if you don't have enough cash to pay your full credit card balance and cover other expenses until you're paid again, you are riding credit card float.

Watch out! You can still ride the float even if you pay off your balance in full every month. If you need to swipe the card even once before your next paycheck comes in, you're riding the float.

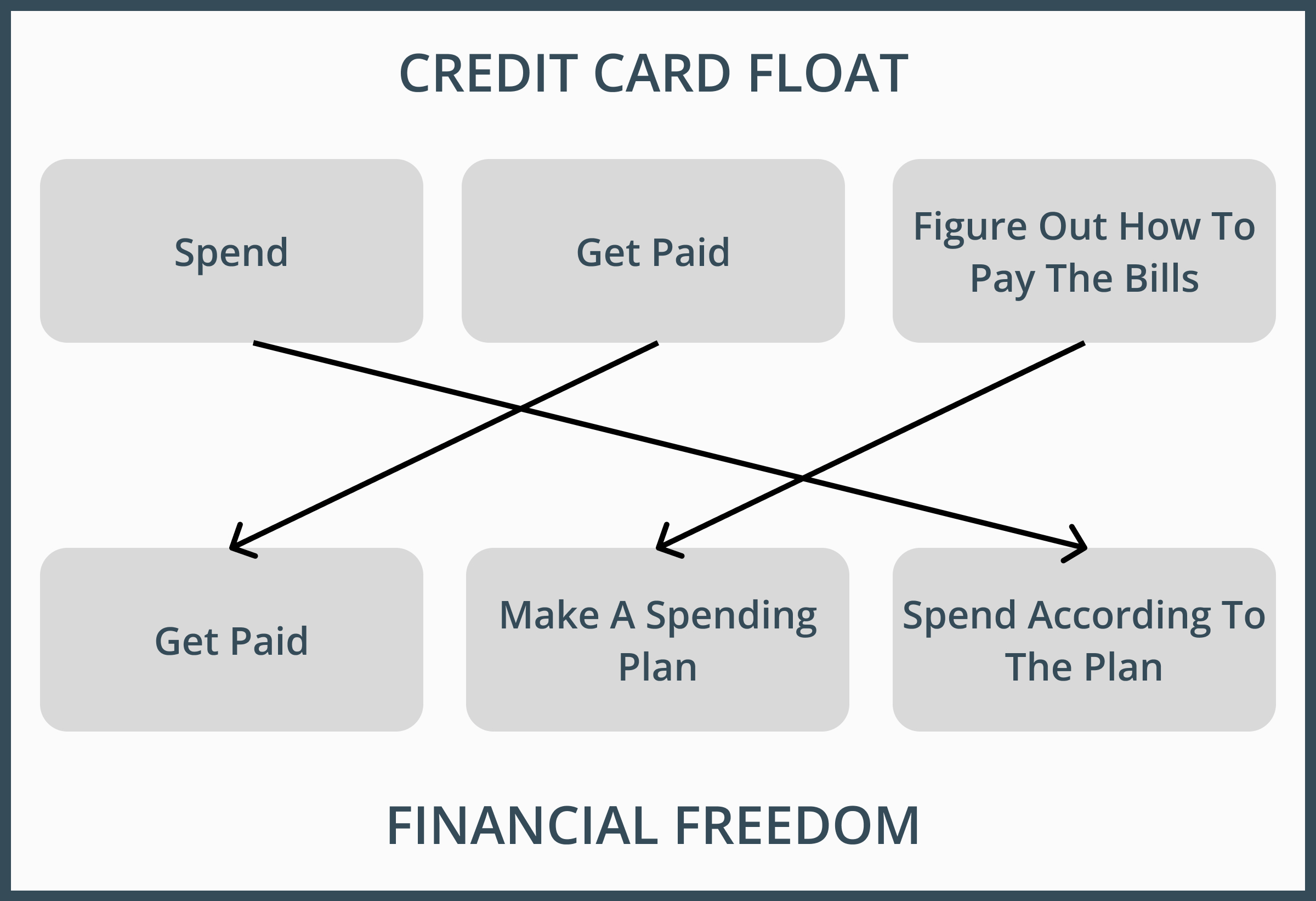

How Do You Stop Riding Credit Card Float?

You got onto the float by spending money before you got paid. The only way to get off the float is to start waiting to spend money until after you get paid. You need to change the order of operations from spend, earn, plan to earn, plan, spend. (Another name for planning your spending is budgeting.) There are two ways to make this happen.

Temporarily Stop Paying Your Card In Full

The fastest way to get off of the float is to stop paying your card in full. Make only the minimum payments. This might sound counterintuitive. You've always been told never to carry a balance. The truth is, if you're riding the float, you are carrying a balance...you're an entire month behind on your finances. You're using money you haven't earned yet to pay for things you bought over a month ago. You may not be paying interest, but you're trapped all the same. Temporarily making minimum payments on your credit card frees up cash to cover your current expenses with your current income. It stops the cycle of adding more debt to your card. Once you've covered your immediate obligations with cash and stopped accruing new debt, you can turn your attention to paying off your credit card balance in full again.

Cut All Unessential Spending

The slower way to stop riding the float is to cut spending on non-essentials and use that cash to cover your immediate obligations. Stop making unessential purchases on your credit card and use that cash to pay for your immediate obligations.

Fixing Your Cash Flow Is Worth It

Both of these methods are hard, but the pain is temporary and the payoff is nothing short of majestic! Financial freedom at last! Ditching a life lived on credit card float is literally the difference between constantly playing catch up and taking control of your finances. You are now in charge. Stick it, credit card.

Understanding Your Credit Card Bill

Most people don't realize that when you make your credit card payment, you aren't paying for the current month's spending or even last month's spending. You're paying for things you bought the month before that! This is because of the difference between your credit card statement closing date and balance due date. Most credit cards give you about a month long grace period after the statement closing date before you must pay the balance for that billing period or begin to pay interest. So, if you spent $2,000 on your card during January and your statement closing date was January 31st, you would not be required to pay the balance from that statement until the end of February! By that time, you could easily have racked up an entire February's worth of new expenses! You can see how easy it is to get a month behind on your payments. Remember, credit card use is debt, no matter how soon you plan to pay it off.

Conclusion

The credit card system is designed to encourage you to buy now and pay later, with interest. It's a slippery spending slope, and without a plan for spending your money, it's easy to fall into the trap of spending money you don't have, especially when it comes to credit cards.

If you need help figuring out a plan to get out of debt, organize your finances, or get control of your money, book a free coaching call with me today. I'll help you create a plan for your money, avoid credit card float, and get ahead on your finances.