YNAB VS EveryDollar: Why I Choose YNAB

Start A 34-day Free Trial Of YNAB.

Everyone needs a budgeting app. The average adult consumer in the United States makes over 70 financial transactions every single month.1 Without a way to keep track of those transactions, it's too easy to lose control of your finances. Controlling your money helps you save money and ensures financial peace of mind. Nothing makes it easier to gain control of your money than using budgeting software to plan and track your cash flow. Yes, you can budget using a spreadsheet, but do you really want to keep track of all your transactions in a spreadsheet? When was the last time you opened Microsoft Excel or Google Sheets on your phone? Was it a joyful experience? Didn't think so. When you get serious about getting control of your personal finances, you'll want to select a budgeting app to help you streamline the process.

You can choose from a wide variety of budgeting apps, but not all of them will make managing your finances easier. You Need A Budget (YNAB) and EveryDollar stand out as some of the most popular budgeting apps, trusted by hundreds of thousands of people to help them organize their finances. And yet, in doing my research for this article, I could not find an in-depth comparison of YNAB and EveryDollar anywhere online. Existing comparisons tend to give a cursory overview of the basic features of each app (spoiler alert: there's a ton of overlap) and draw ambiguous or oversimplified conclusions. For example, a common conclusion I found is that "YNAB is complex and best for detail oriented people and EveryDollar is simple and best for budgeting beginners." I disagree with this conclusion. Budgeting your money requires attention to detail regardless of which app you use, and frankly, neither app is much simpler than the other. Choosing the right budgeting tool could mean the difference between giving up or sticking to your budgeting habit forever. So, I decided to make my own comparison and discuss the real differences between YNAB and EveryDollar.

TL;DR - YNAB Has More Features, More Flexibility, And More Polish

Start A 34-day Free Trial Of YNAB.

Both YNAB and EveryDollar enable you to budget your money, but four key differences make it a no-brainer to recommend YNAB over EveryDollar for most individuals and families. First, EveryDollar does not allow you to track credit card spending. It is also against EveryDollar's policy to pay for the app with a credit card. This lack of credit cards support is a non-starter for anyone who uses them to make purchases. YNAB not only allows you to track credit card spending, but handles it in a way that reflects what really happens when you swipe your card. Second, YNAB enables you to effortlessly move money between budget categories. EveryDollar makes moving money between categories a cumbersome process. This makes EveryDollar a hard sell for anyone who has trouble sticking to a strict budget (aka all of us). Third, it's much easier to add transaction in YNAB than it is in EveryDollar. Finally, YNAB's product maturity and focus lend it a higher level of polish which reduces friction and ultimately makes it the easier app to use.

Remember, the most important factor in choosing a budgeting app is ease of use. The easier you can track expenses and change your budget, the more likely you are to stick with it, even when your plans change. The easier you can make your budget reflect the reality of your finances, the more likely you are to be honest with yourself about your priorities and spending. YNAB's overall user experience and polish make it much more likely you'll stick to your budget and ultimately win with money.

In the rest of this article we'll take a deeper look at the philosophies that underlie each app, their features, and their pricing.

Already a YNAB customer? Learn where to find your referral link and earn a free month of YNAB.

YNAB VS EveryDollar: Budgeting App Philosophy

Why talk about philosophy in a budgeting app comparison? Because a company's beliefs about budgeting influence how they design their apps. At their core, budgeting apps are just spreadsheets or databases for planning and recording your financial transactions. You'd expect their feature sets to overlap quite a bit, and they do, as you'll see in the features comparison below. While both apps enable you to budget your money, they are created by two very different companies with different focuses and approaches to budgeting. These different approaches make for very different user experiences.

Zero-Based Budgeting

Let's start with what these apps have in common. Both apps encourage you to assign every dollar a job. People often refer to this concept as zero-based budgeting. The first of YNAB's 4 rules is: "give every dollar a job." EveryDollar uses this same phrase as one of its taglines. The similarities between these two apps pretty much end here.

Company Focus

The YNAB app comes from a company called You Need A Budget LLC. The company exists solely to help people gain control of their money by teaching them to budget. YNAB has its own unique approach to budgeting, which it calls the YNAB Method, which consists of 4 simple rules. YNAB designed its budgeting app to make following those rules very easy. YNAB does not prescribe how you should spend your money. Instead, it acknowledges that you can use the inherent scarcity of money as a tool to discover and make choices about your true priorities and spend your money accordingly.

EveryDollar is built by Ramsey Solutions, a company founded by Dave Ramsey and made famous by his Financial Peace University and 7 Baby Steps. Ramsey Solutions is not a budgeting company. It is a personality-driven media company. It offers a wide variety of products and services from workshops and other live events to books, coaching, and a network of affiliated financial advisors, insurance and real estate agents, and so on. Although Ramsey Solutions supports budgeting as a foundation of personal finance, you won't find "budgeting" in Dave Ramsey's 7 Baby Steps. EveryDollar's philosophy could be summarized as, "debt is bad; pay cash for everything." The app is built to encourage you to follow Dave Ramsey's Baby Steps. It seeks to influence users to spend money in accordance with the 7 Baby Steps, which makes it a bit more prescriptive than YNAB as both method and a software.

YNAB VS EveryDollar: Credit Cards

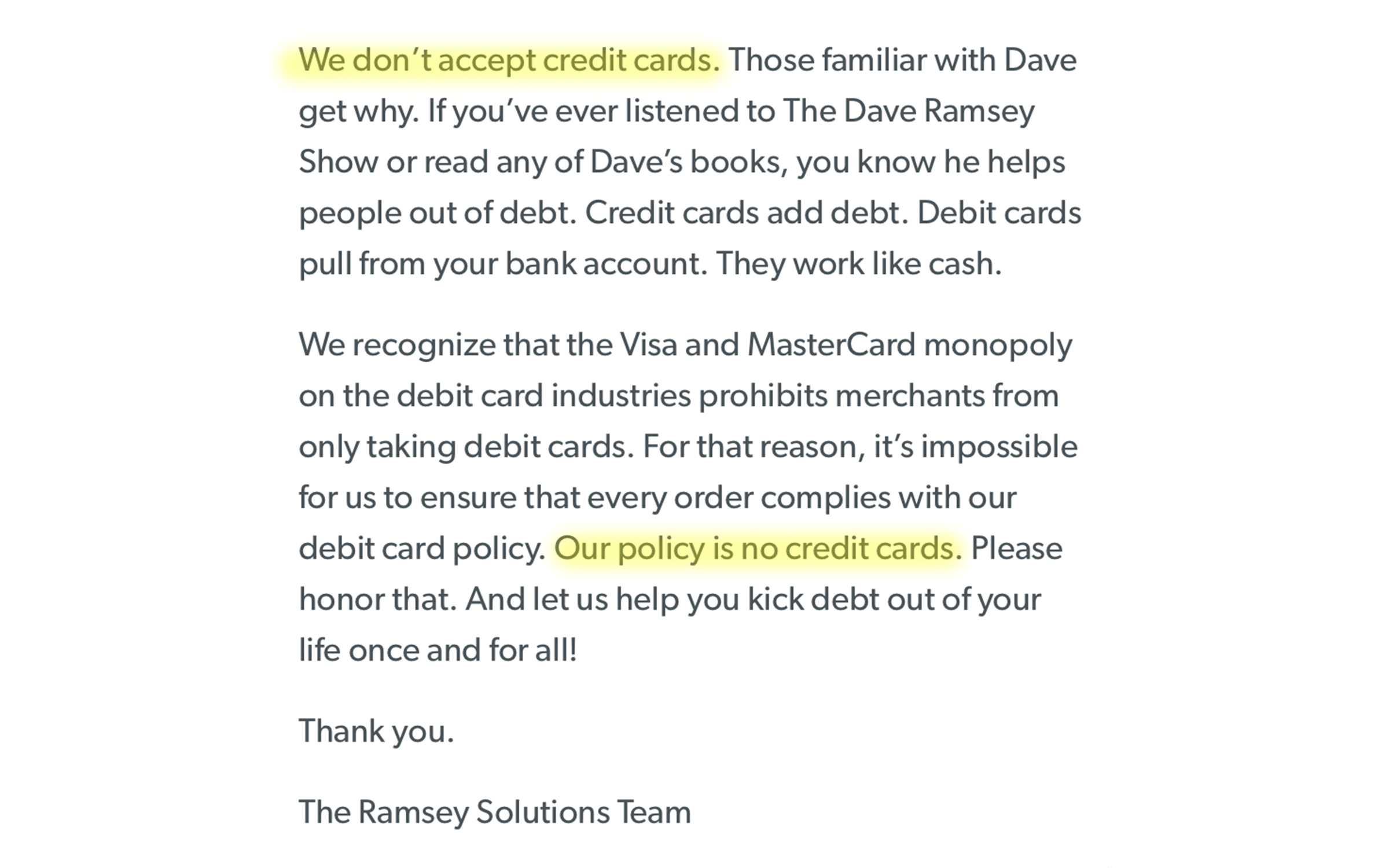

Dave Ramsey's EveryDollar app does not support credit card accounts. Use a credit card? Too bad, you won't be able to add your credit card account to your EveryDollar budget. Ramsey Solutions takes their anti-debt approach very seriously, which I admire. But if you are one of the more than 80% of Americans who use a credit card to make purchases, you should not choose EveryDollar as your budgeting app.2 In fact, Ramsey Solutions does not even allow you to pay for your EveryDollar subscription using a credit card.

YNAB, in contrast, embraces the realities of credit card usage better than any budgeting app I have ever tried. It mirrors the reality that swiping your credit card is equivalent to taking out a loan for the amount of your purchase, but doesn't record money leaving your budget until cash actually goes out to make your credit card payment. Do you have a credit card balance? YNAB includes a loan payoff calculator and goal features to help you pay off unwanted credit card debt if you carry credit card balances. Properly accounting for credit card use is key to preventing credit card debt and getting off of credit card float, which is why I wrote this article about how to beat credit card float.

Debt Repayment

Speaking of debt, Ramsey Solutions has an aggressive approach to debt repayment. After you've cut up and stopped using all of your credit cards, they encourage you to save a $1,000 emergency fund (Baby Step 1). After that, the company encourages you to dump every spare cent into paying off your debts...all of them...until they are gone. EverDollar reflects this philosophy and is designed to facilitate this approach.

YNAB has a similar but more flexible approach to debt repayment. They encourage saving for your true expenses (YNAB Rule 2) as you work to pay down your debt. While it may seem like you'd get out of debt more slowly this way at first glance, YNAB embraces your inconsistent human nature and sets you up for success in a different way. By encouraging you to save consistently for these expenses, they know you'll more likely have cash on hand when something goes wrong or your priorities change. This means you're far more likely to stay on track. You might just pay your debt off just as fast as the Ramsey method because you'll be avoiding setbacks when surprises happen. At least that's the idea. That said, YNAB doesn't prevent you from paying down your debt with intensity if you want to (it has loan payoff tools that EveryDollar doesn't, like a calculator to show you how much time and money you'll save by making extra payments). YNAB's more slow-and-steady approach prioritizes avoiding new debt by encouraging you to save more along the way.

Forecasting

Aside from EveryDollar's credit card ban, forecasting is probably the biggest difference between the two apps. YNAB does not allow you to forecast, while EveryDollar is essentially a forecasting tool. What does this mean?

YNAB's first rule is "Give every dollar a job." That's also one of EveryDollar's taglines. Remember, both apps are zero-based budgeting apps. However, YNAB only allows you to assign jobs to dollars that you already have, literally right now, literally sitting in your bank account. You can't make plans for money you don't have yet.

EveryDollar, on the other hand, encourages you to make plans for money you don't have yet. In fact, one of its major features is called Paycheck Planner, where you enter your future paychecks and begin to allocate them to your budget categories ahead of time.

There are decent arguments to be made for each approach, but I think YNAB wins here, too, for two big reasons. First, YNAB acknowledges the reality of human nature. They basically say, "It's hard enough sticking to your plan for the money you have today. Are you really going to accurately predict how you'll spend money you don't even have yet." I like apps that recognize and take advantage of the path of least resistance because that means you're more likely to stick with a healthy budgeting habit, and I think this is one example of YNAB doing that brilliantly.

The second, and perhaps more important reason to favor YNAB's lack of forecasting over EveryDollar's paycheck planning method is the psychological effect of scarcity. YNAB puts you face to face with the reality of how much money you actually have. For many beginning budgeters, that amount will not be enough to cover all their expenses right away. This forces you to answer the question, "What do I need this money to do until I get paid again?" If you don't have enough money to cover a full month of expenses, you will find out really fast what you truly value, and you'll be highly motivated to "age your money" (YNAB's Rule 4) so you can get a month ahead and break the paycheck to paycheck cycle. This approach works for people on any pay cycle--bi-weekly, monthly, twice a month, etc. It's also an ideal approach for freelancers, business people, and others with irregular or unpredictable income who would likely find EveryDollar's focus on paycheck planning to be limiting and frustrating.

Ecosystem of Services

Finally, it's worth addressing the ecosystem in which each of these apps reside.

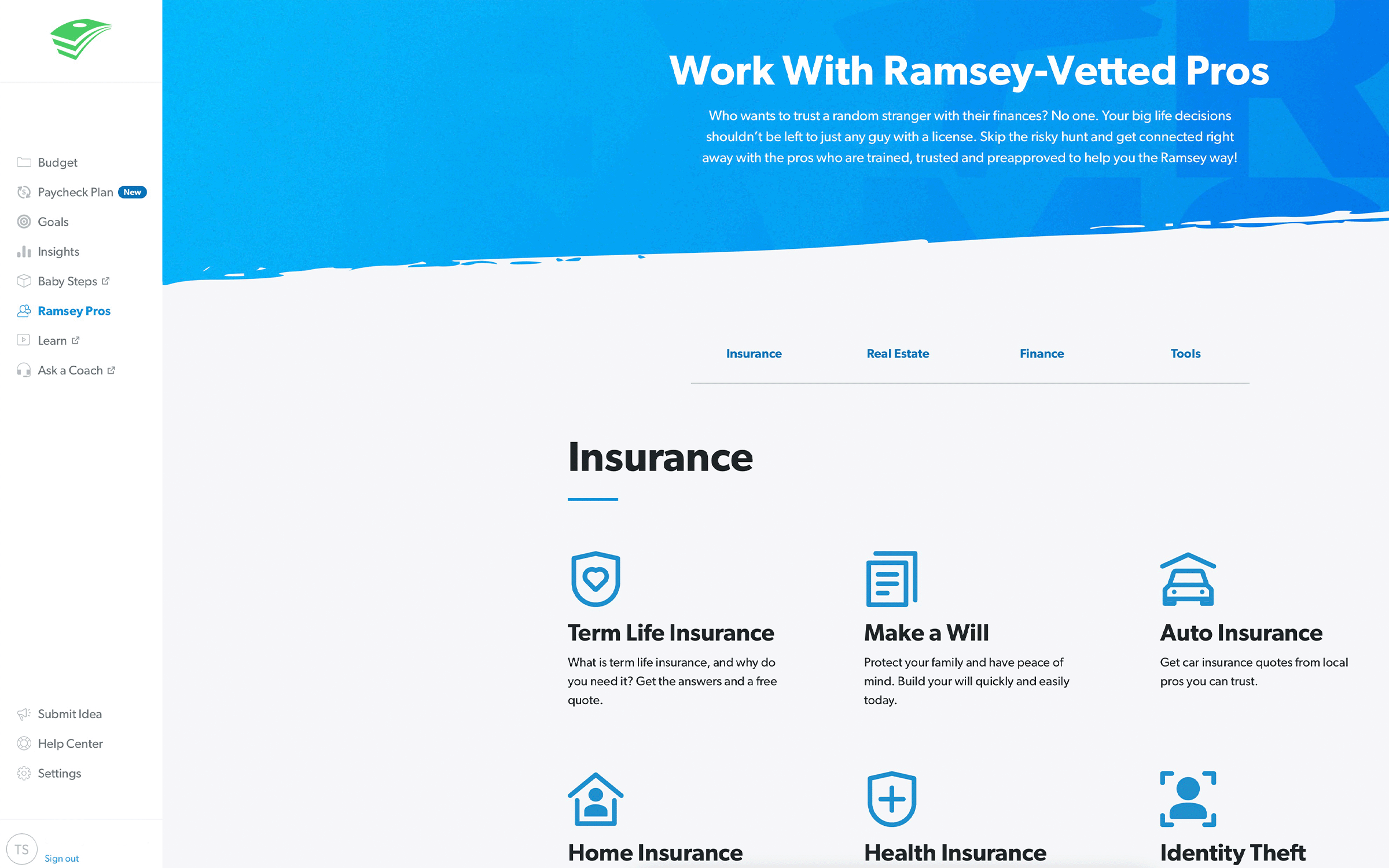

EveryDollar is part of a much larger business model. Inside of the app you will find advertisements for Ramsey Solution's endorsed providers and sections devoted to helping you purchase almost any financial-related services you can think of: insurance (auto, life, home, and many more), real estate agents, mortgages and loans (kind of ironically?), investing and financial advisement services, and coaching. It's kind of a lot, to be honest. Paired with how often Ramsey Solutions pushes these affiliates and services on their radio, podcast, and YouTube programs, it seems obvious that selling them is a huge part of their business. Nothing wrong with that, just important to keep in mind that budgeting is not the sole or even main focus of the company that makes EveryDollar.

YNAB, on the other hand, is simply a budgeting company. They have a solid methodology that helps people get good at managing their money, and they have an app that is laser focused on the same thing. The company puts its full weight behind a single purpose: helping people master their money with the critical life skill of budgeting.

It is worth noting that group coaching is included in EveryDollar's subscription fee. If you want to hire a YNAB Coach, you can find one in YNAB's Certified Coach Directory, but you'll need to pay for their services separately as they are not YNAB employees.

YNAB also produces excellent help resources and tutorials.

YNAB VS EveryDollar: Features

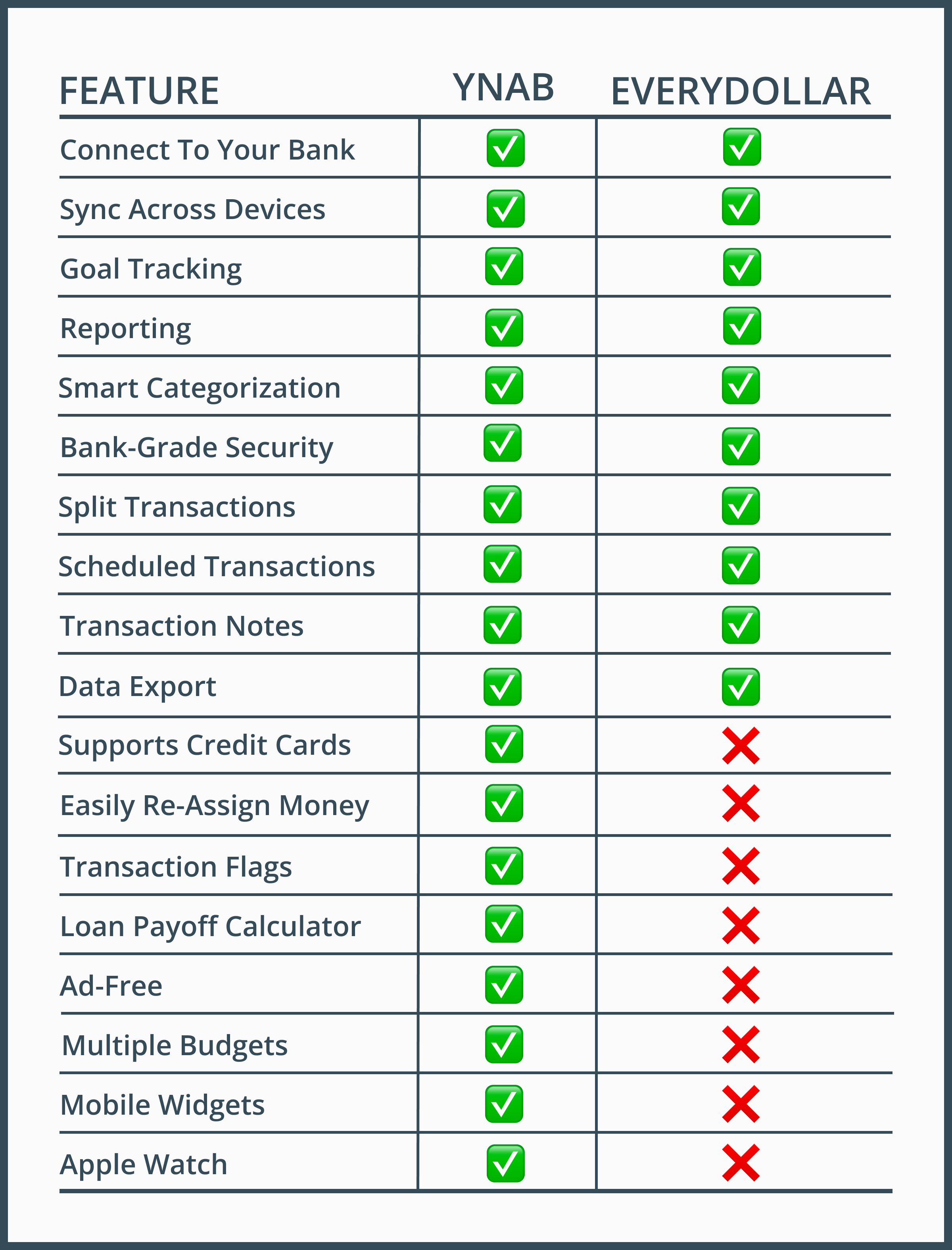

With all that talk of philosophy out of the way, we can finally turn to feature comparison! YNAB and EverDollar share many features, even if they implement them differently. Overall, YNAB has more features, as illustrated in the following table. Below the table, I'll outline a few feature-based differences between the two apps that I feel make a significant difference in user experience.

YNAB VS EveryDollar: Feature Comparison

In addition to the features listed above, YNAB recently launched a new feature called YNAB Together, which is essentially a family plan. For the price of a single subscription, you can invite up to 5 additional users, each with their own accounts and login information. Each user can create and manage their own budgets. This feature makes sharing a household budget with a partner, spouse, or roommate extremely easy! It also provides an ideal solution for teaching your children how to budget or helping to manage the budget of someone for whom you are a caregiver.

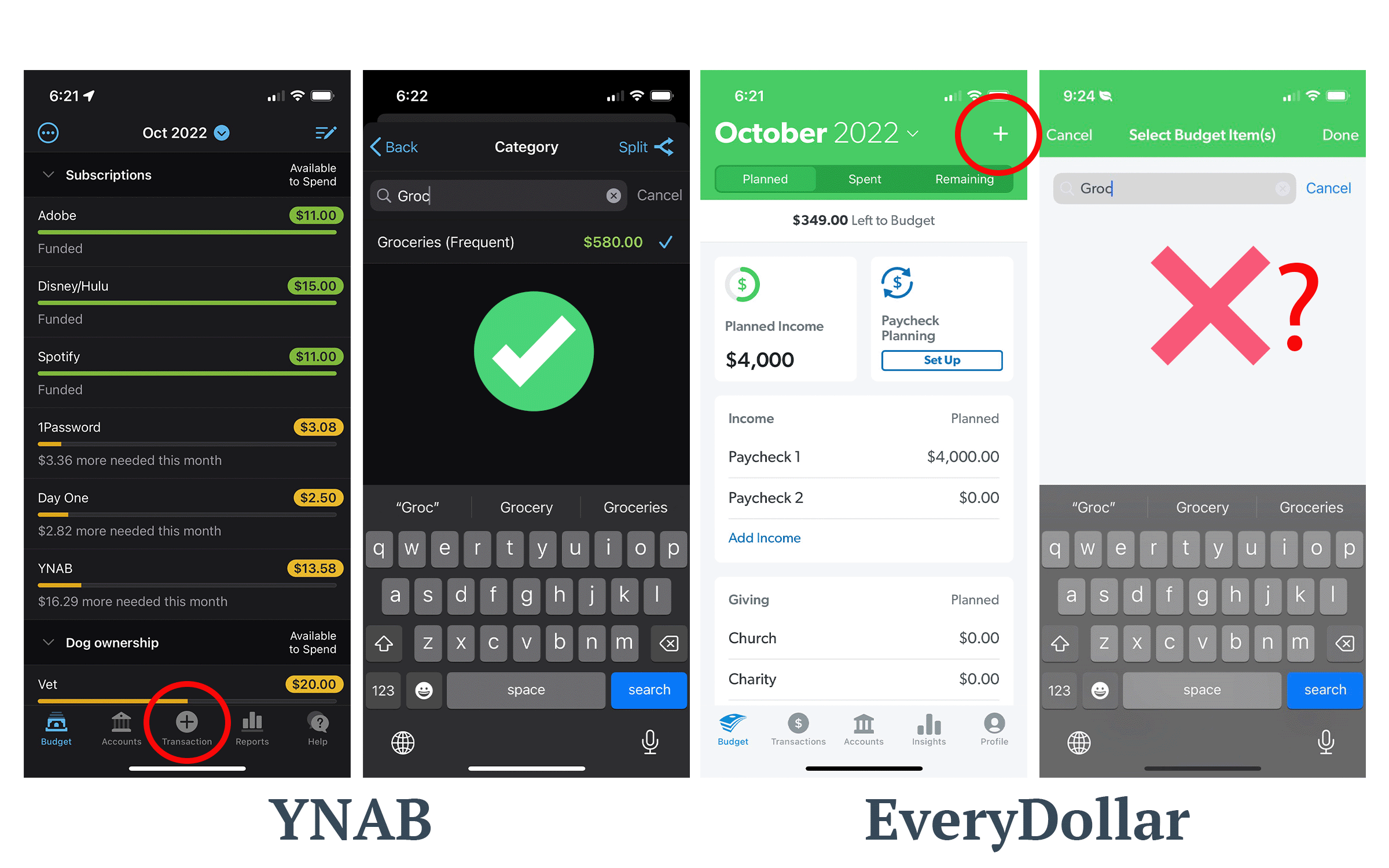

Ease Of Adding Transactions

Winner: YNAB

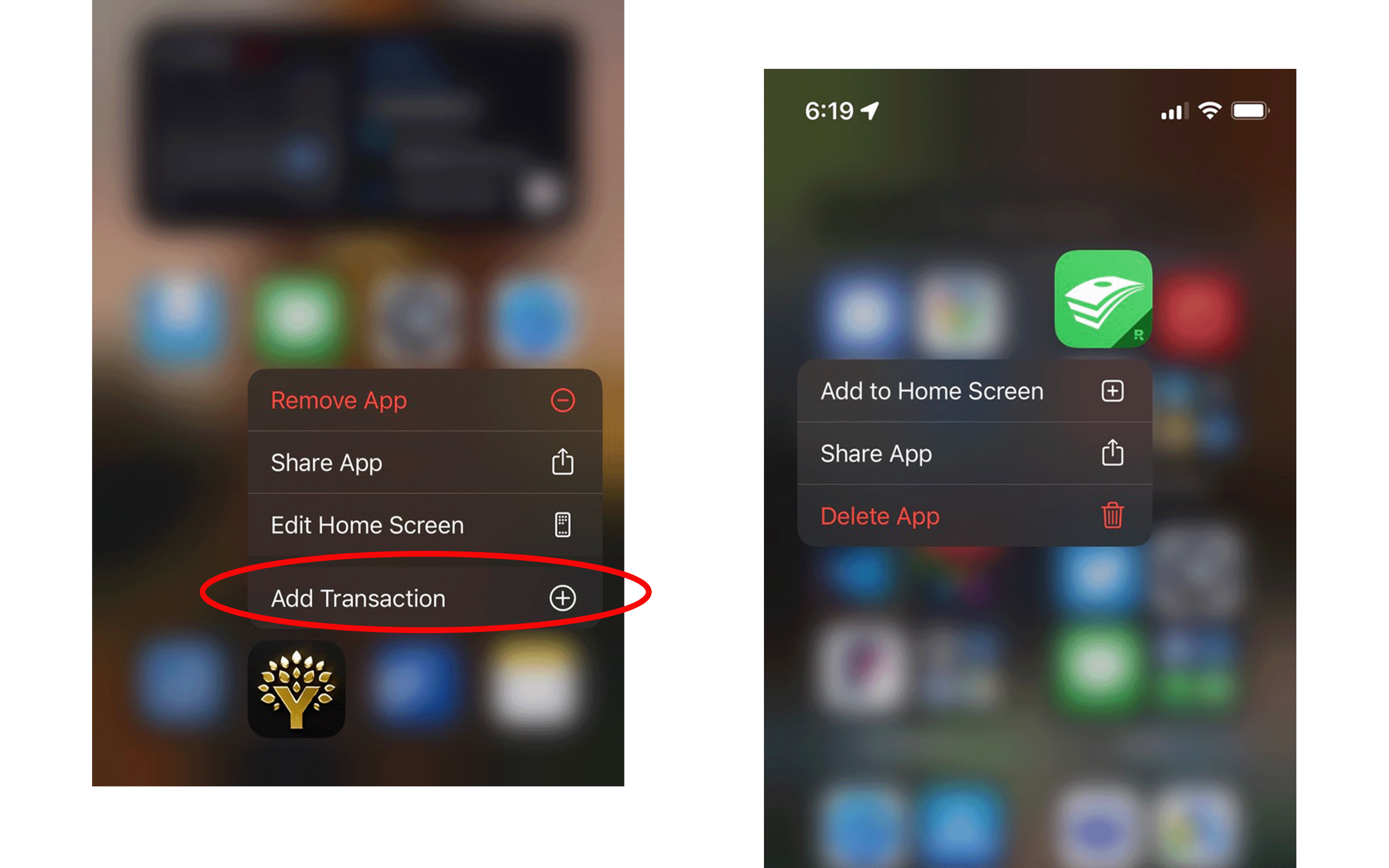

On mobile, you can quickly enter a transaction in YNAB by long pressing on the app icon. If you are using a mobile widget, you can quickly enter a transaction by clicking on a category in the widget. EveryDollar does not support quick add by long pressing on the app icon and does not have mobile widgets.

From within the mobile app, the add transaction button is placed way at the top of the screen in EveryDollar while it is conveniently front and center at the bottom of the app in YNAB.

YNAB has location-based payee suggestions, EveryDollar does not. If you've chosen to share your location with YNAB it will detect your location when adding a transaction, and if you've added a transaction there before, it will pre-populate the payee, saving time.

In what seems like a bug, EveryDollar does not auto-suggest categories for your entries as you type. Very annoying.

Flexibility

Winner: YNAB

YNAB knows you won't stick to a budget that's too strict. That's why their third rule is "Roll With The Punches." Accordingly, YNAB makes it very easy to move money between categories when your priorities change or to cover overspending. YNAB also surfaces an in-app notification when you've overspent a category. It prompts you to cover that overspending with money from another category, which is easy to do with a single touch.

EveryDollar does not have these features. If you want to move money between categories in EveryDollar you must subtract it from the desired category, which sends it back to the "left to budget" status. From there you have to re-assign it to another category. Very annoying.

Polish

Winner: YNAB

YNAB is just the more mature app, especially when it comes to the little things. It supports dark mode fully and has several color themes to choose from. On mobile, you can choose from a variety of app icons. I obviously chose the "bling" icon. Additionally, YNAB automatically carries your monthly budget over to the next month while EveryDollar requires you to manually create next month's budget.

Additional Feature Notes

Both YNAB and EveryDollar (paid version) have similar reporting available so you can visualize your spending habits: spending money totals and trends by category. YNAB has one report that EveryDollar does not--a net worth report. YNAB also allows you to set custom date ranges on your reports while EveryDollar has preset time periods.

YNAB and EveryDollar both support savings goals, but they handle this differently. In YNAB you create financial goals by setting targets on existing categories. EveryDollar handles financial goals as separate categories altogether.

Pricing

How much does YNAB cost?

YNAB costs $14.99/month or $99/year and comes with a 34-day free trial.

How much does EveryDollar cost?

EveryDollar costs $12.99/month or $80/year and comes with a 14-day free trial.

You will save money significantly on both apps by opting for an annual subscription instead of monthly billing.

Is There A Free Version Of The Budgeting Apps?

YNAB does not have a free version. The EveryDollar app does have a free version. However, the free version has so few features that I can't seriously recommend it for anyone looking to develop a healthy budgeting habit in their life. For example, the free version of EveryDollar does not allow you to connect your checking accounts, savings accounts, or other financial accounts and automatically import transactions. If you choose to use EveryDollar, you will definitely want to use the paid version. In my experience, you get what you pay for, and free budgeting software is unlikely to provide a delightful experience.

Conclusion

You Need A Budget (YNAB) is really the best budgeting app for most people. It has more robust features, smoother, more convenient design, and a ubiquitous app experience, all built to help you follow a simpler, more flexible method for managing your money.

Start A 34-day Free Trial Of YNAB.